The Employees’ Provident Fund (EPF) of Malaysia has long been criticised for offering a one sized fits all retirement savings solution for all Malaysians. It has only one fund for all its contributors aged from the 20s to 50s. Everyone gets the same return every year.

Ideally, younger contributors should be able to put their savings into riskier investments to reap higher returns while older contributors should rebalance their investments to safer ones to protect their savings.

In 2012, some smart consultants must have seen the opportunity to propose to the Najib government to set up an alternative retirement savings scheme called the Private Retirement Schemes (PRS). In general, there are 3 types of PRS funds, ie growth, balanced and conservative. Growth funds will hold more stocks (riskier but higher returns), while conservative ones will hold more bonds (safer but lower returns). Balanced funds are somewhere in the middle.

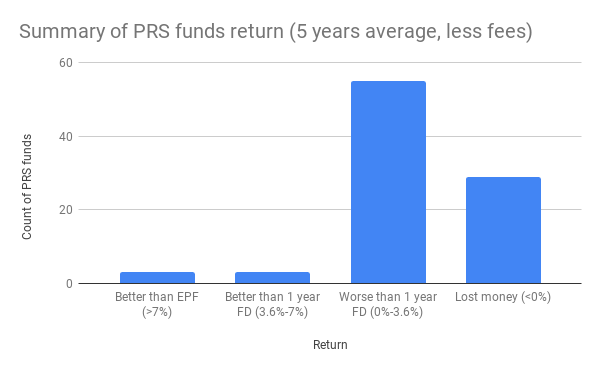

The idea sounded great but 6 years down the road, we can now see how terrible their long term returns are. From Morningstar, I could find 90 PRS funds with data. 70 of them have been around for at least 5 years. Take a guess what the median return is for the 90 funds.

It’s 3.17%. That’s no better than putting your money in the fixed deposit.

Now all these funds are actively managed so they charge fees, such as sales fees, management fees, trustee fees and redemption fees. If you read my posts you will know that I really have a distaste for high fees. Now take another guess what the median return is after deducting the fees.

It drops to a measly 0.94%! The fund managers gladly pocket their fees and leave you high and dry come retirement day.

Here is the spreadsheet with the details.

Only the CIMB-Principal PRS Plus Asia Pacific Ex Japan Equity fund performed better than the EPF by returning over 7% on average. The only reason the fund performed better than EPF is because it’s fully invested in stocks. And unlike most of the pure equity funds in the PRS, it’s buying stocks outside of Malaysia which makes it possible to get a higher return than the KLSE.

The Manulife PRS funds charge the highest management fee out of the whole lot, up to 2.25% per year. Surprised, I checked what they bought and it looks like they are also the laziest because they simply repackage their own funds into their PRS funds. It’s therefore not a surprise they ended up with the highest management fee because of the double charging of management fees coming from funds within the fund.

By now, it should be clear that PRS funds are a retirement money sucker. Keep your money in the EPF or a diversified ETF until the PRS funds get their act together.

Note! There is a high chance that the EPF will declare a lower dividend than usual for 2018. But I would bet that it’ll still be better than that of the majority of the PRS funds.