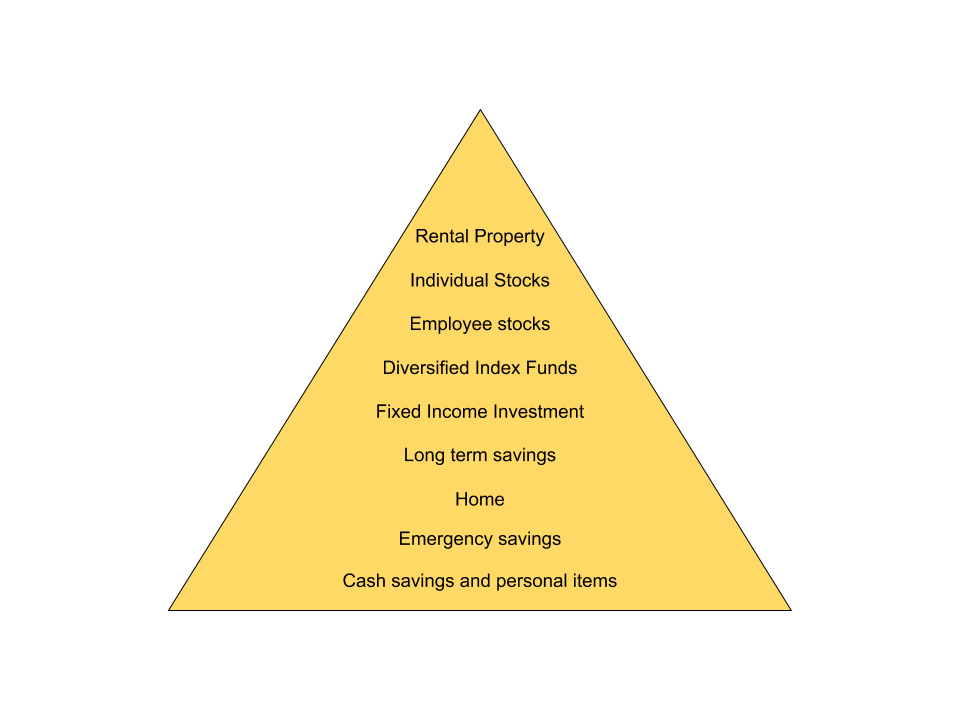

We are now approaching to the top of the asset allocation model and the ninth layer concerns properties bought for the purpose of investment. I mentioned that the risks involved with investing increases as we go up the layers of the model. I’ll talk more again about the risks associated with property investments later on.

It is true, at least in Malaysia, that people are drawn to properties because of the prospect that ‘property prices never come down’. While that is true in many places across Malaysia, the recent property glut has cast a cloud of doubt over the minds of many would-be investors.

The answer to the question on the minds of these folks is that property prices can come down. It has already happened for certain areas but the situation is not as bad as 1998 and 1999. Over the long term however, not many remember the price declines of 1998/1999 because prices have recovered and continue to increase since then.

The following post focuses on investments in RESIDENTIAL properties. The risks and gains for commercial properties are different but that’s probably a topic for a different post.

Property Investing Is Not The Same As Buying A Home

If you are going to be a serious property investor, it’s important to establish your main reasons why you are choosing property as an investment asset. Are you looking for a reassuring steady flow of rental income to supplement your monthly cashflow? Are you enticed by the meteoric rise in property prices and want a piece of that action? Or have you been mesmerised by that property brochure that you picked up at a property show house and thought ‘wow, that’s a very nice place to live in and maybe someone would want to rent it from me’.

You can have many reasons but if you have reasoned from your heart rather than your brain, then there is a good chance that you are going to make the wrong choice. This is because property investing should be more like making a business transaction than buying a home. There is a difference between the two!

A property investor will seek to maximise his/her returns from the business transaction. That means buying a property at its best value, improving that value with as little capital as possible, and then renting or selling to realise the highest possible value for him/herself. I’m sure you are not thinking like this when you are choosing to buy your own home.

Rental Properties – Increase Your Chances Of Success by Putting On Your Business Hat

One primary objective of any business is to have the ability to sustain positive cash flow. Any business that is losing cash over time will eventually close down. And it makes sense to think about investing in property the same way.

First consider your cash outflows.

- When you purchase a property, your immediate cash needs are the booking fee and from there the rest of the downpayment by the time the sales and purchase agreement is drawn up. This can come from your own savings or even partially borrowed from the property developer.

- If you purchased a property that already exists (ie buying from the secondary market), then there will also be legal and stamping fees to consider. These miscellaneous costs can come up to 5% of the purchase price.

- You will also likely take a home loan to finance the remainder of the purchase price. Servicing the home loan means a monthly cash drain to pay the interest and principal. You can reduce this as much as possible by comparing between banks and getting the best rate that you can qualify for. You should also get the longest possible loan tenure since that will give you the lowest monthly payment.

- You may also need to spend some money to do some minor repairs or renovation to the property. If you choose to rent out your property, you may need to furnish the property as well (as furnished homes get better rental). As these are again cash outflows, you would want to have a budget ceiling and not overspend.

- Some properties will have regular monthly costs like maintenance fees and sinking fund. Also don’t forget the quit rent, assessments and periodic maintenance like plumbing repair and servicing the air conditioner.

It’s generally easier to spend money than to earn it. So now you need to really make sure that your property can generate enough cash inflow over time to offset your cash outflow. One approach is to target specific groups of people who are more likely to rent a property than to buy one themselves. This will ensure that you have a constant supply of tenants looking for your property.

- Private college or university students. Some people partition their property spaces to create as many ‘rooms’ as possible to be rented out to private college or university students. Young students don’t require fancy furnishing but they can be demanding these days about other amenities like free internet, washing machine, air conditioning and gas stove. Rental income can be high but that’s to offset the occasional property and furnishing damage as well as runaway unpaid electricity bills. We are talking about young kids here and their lives are full of risks, some of which are passed on to you.

- Tourists. Airbnb offers an amazing democratisation of rental properties these days. If you have the energy and a sunny personality, you can list your property on the platform and get pretty good rental income for short stays. The downside is that competition can be intense in terms of rental price and tasteful furnishing. Additionally the income is irregular and you need to find a way to be able to constantly clean up and prepare the property for the next visitor.

- Expats. Expats can afford pretty high rents but they also generally look for established expat neighbourhood that is safe with good facilities such as reputable international schools. These kinds of places carry a premium price tag as such. Additionally, expats come and go and the last time when the oil price crashed in 2016 plenty of oil and gas expats left the country.

- Young singles or families. Young folks just starting out working will more likely rent than buy their own home. They may choose a location that’s near their work place or near an LRT/MRT/Komuter station for convenience. Over time, they may move out when their family grows but if the property is located in a good location, there should be new tenants looking at your property.

Getting To Positive Cash Flow

To minimise the initial cash outflow, you want to be able to rent out your property as soon as possible. In an ideal world, your property would come with ready tenants. You can engage an honest and reliable property agent to help you out with this or DIY via several of the property listing websites available.

At the end of the day, the cash inflow needs to exceed the cash outflow for your property investment to be cashflow positive and succeed. The exception to this is perhaps the downpayment that you paid initially, since this forms part of the property value that you immediately own (its equity value). Depending on how much you have spent to prepare the property for rental (including legal/stamp duties if any), it could take several years to break even on your cashflow.

Obviously being cashflow positive also means that you don’t have to ‘top up’ on the cashflow needs from your other income sources. That means that your property is self-sufficient – even if you lose your job or your other income sources, you won’t be forced to sell your rental property.

You may wonder why I have not considered the appreciation of the property value over time. After all, price appreciation over the long run is a big reason why people invest in properties.

The short answer is that price appreciation, although itself can be very substantial in value over time, isn’t something that you can count on immediately to pay for your home loan payments or plumbing repairs. It does not produce cashflow immediately.

You can only realise the price appreciation if you sell the property (kill the golden goose?) or refinance your home loan (which may be constrained by the lock in period). The fact is that you may only sell the property if you manage to find another property that has potentially more positive cashflow than your current one or refinance when the bank interest rates have dropped below that of your current home loan. But both of these events do not come by often.

To be clear, when the property value increases over time, and as you make your monthly loan payment, your equity in the property increases. As an investment asset, this then adds to your nett wealth although it does not contribute cashflow. Bluntly, it looks good on paper but all that doesn’t matter if you cannot keep up with the cash outflow (loan payment + expenses). This is why it is important to make sure that your cashflow is healthy before you consider the potential price appreciation. Call the price appreciation the big icing on the cake that rewards the patient investor.

Capitalising on Short Term Capital Gains

There is another form of property investment that takes the form of buying a property during its construction period and then quickly flipping it once the keys are handed over.

During the go-go years of 2010, 2011 and 2012, that were fuelled from 2009 by low bank interest rates, a 0% real property gains tax (RPGT) and rampant developer interest bearing scheme (DIBS) financing, property flipping was a buzzword.

There may have been people who succeeded in this but just like momentum investing in stocks, it works when there is a large supply of people trying to get into properties irregardless of price (due to the favourable financing). Right now however, the trend has reversed and a large number of properties are unsold. It’s probably not a good strategy for the current period.

What Can Go Wrong With Property Rentals?

Renting out properties does not work on autopilot. Neither is it stress-free. Below are some of the things that can and do go wrong:

- Non-payment of rental. Tenant starts by paying the rental late and before you know it, the rental no longer comes in. A sob story from the tenant is to be expected at this point.

- Non-payment of electricity and water bills. You see the bills going up and up and there is no sign of payment. If you are not careful, the outstanding amount will soon exceed the utilities deposit. (You could avoid this for the TNB bill if you change the account to the tenant)

- Constant maintenance. Call it luck but there is a never ending bout of maintenance problems coming from the tenant. If it’s not a leaking air conditioner, it’s a blocked plumbing or leaking from the ceiling. Sometimes a piece of the furniture breaks off or the TV breaks down.

- Surprise damage of property and furniture upon moving out. You hear no complaints from the tenant but get a nasty surprise when they move out as you discover that your place is trashed. You wonder if the deposits will cover the repairs.

- Unable to find tenants. If you are unlucky enough to buy a property in an unpopular location, you may spend months trying to find a tenant. No cash inflow, only cash outflow.

REITs – A Stress-free Solution to Property Investing

A REIT or real estate investment trust is essentially a company listed in the stock exchange that owns and manages one or several properties. The company earns revenue by renting out the properties and distributes the income periodically to the shareholders once it’s deducted the operating expenses and management fees.

In Malaysia there are almost 20 REITs listed on the KLSE. They hold properties like shopping complexes, offices, factories, hospitals and hotels. Some of the properties are highly recognisable, such as the KLCC, Sunway Pyramid, Midvalley and Pavillion shopping complexes.

The advantage of REITs is that you can buy a small share into these properties through the stock exchange and receive ‘rental income’ in the form of dividends from the companies. The management takes care of the tenants on your behalf. There is no need to save up for downpayment and no loans to apply for. The minimum amount needed is just the value of 100 shares.

The downside is that the capital gains may potentially be less since it will be limited by the number of shares that you own. In the case of buying properties, you only pay a portion of its price initially but stand to gain from the rise of the entire property value.

Performance of REITs

It may come as a surprise that some REITs perform better than the average KLCI returns and potentially even better than owning an actual property.

Say as an example, you bought a high rise investment property worth RM400,000. You paid 10% as downpayment and took a 90% loan at 5% interest for 30 years. This results in a monthly instalment of RM1,933.

You paid an addition 5% for the legal fees and another 5% to furnish the property with curtains, furniture and appliances. Your total initial cash outlay is RM80,000 (RM40,000 for the downpayment and the rest for legal and furnishing).

Let’s also assume that you found a tenant that pays you exactly RM1,933 every month for rent. That way you are cashflow neutral as technically your tenant pays the monthly loan payment for you. Also let’s assume that the property value increases at 5% per year. (A very generous assumptions since the historical median for high rise property value appreciation is less than 3%)

Your property equity value (paper gains) less the RM40k sunken initial outlay for legal fees and furnishing by year is as follows:

| Year 1 | RM 26k | Year 6 | RM 176k |

| Year 2 | RM 53k | Year 7 | RM 211k |

| Year 3 | RM 81k | Year 8 | RM 247k |

| Year 4 | RM 111k | Year 9 | RM 286k |

| Year 5 | RM 143k | Year 10 | RM 326k |

Looks impressive doesn’t it? Now let’s compare it with the performance of the Pavilion REIT (PAVREIT).

I know it’s apples and oranges but since there are no residential REITs, this will have to do. In the end if you don’t think the performances can be compared, just consider the performance of the REIT on its own.

Pavilion REIT was listed on December 2011 at a price of RM0.88 a share. Since then and up till last February it has paid out a total of RM0.8666 in dividends per share. Additionally its current share price is RM1.73, a 97% gain from the IPO price. If you include the dividends, the total gain would be 195% over 7 years.

If the RM80k was invested in Pavilion REIT at its IPO 7 years ago it would be worth RM236k now which is slightly ahead of the gain from the property investment.

Certainly there are REITs that underperform Pavilion REIT and there are also others that perform better. But the allure of REITs here is the fact that you are able to own a piece of a property without the hassle of managing one.

What To Do Now?

It’s up to your own preference and style. Some people prefer to own a tangible asset rather than paper stocks. These people may look forward to the drop of property prices since that will improve their cashflows (possibility of cheaper loan instalments and hopefully the rent prices holds).

But as with any investments, be aware of the risks, and do your research. Websites like Edge Property offer very good insights of past transacted prices of popular areas. You will find that not everyone profits from property sales and this is before taking into account sales commissions and legal fees. Investing in property is certainly not a sure thing if you are not careful.