As I write this article we are less than 2 weeks away from the doorsteps of 2020.

It has also been a year since I started financedurian.xyz. How time flies when you are not paying attention.

The purpose of financedurian.xyz is to distill all my experience and knowledge in personal finance and investing into a form that’s hopefully not too difficult to understand but more importantly free from the marketing biases that you will typically encounter when reading and learning about these topics. This website is not affiliated with any financial companies, so I will tell things as how I perceive them.

Sometimes the message will not be so nice, hence the durian name of the website.

The ideas behind the contents of financedurian.xyz are not new. They are simply and usually drowned out by the louder voices of the financial news and advertisements that we hear, stirring up emotions that drive people to buy or sell on impulses rather than by sound reasoning.

Is 2019 really such a bad year for the Malaysian stock market?

The KLCI is currently down 3.5% in 2019. The rhetoric that you will hear in the news is that this is due to the US-China trade war, the slowing down of the global economy especially in Europe and the fragile financial markets as evidenced by the negative government bond yields in several countries.

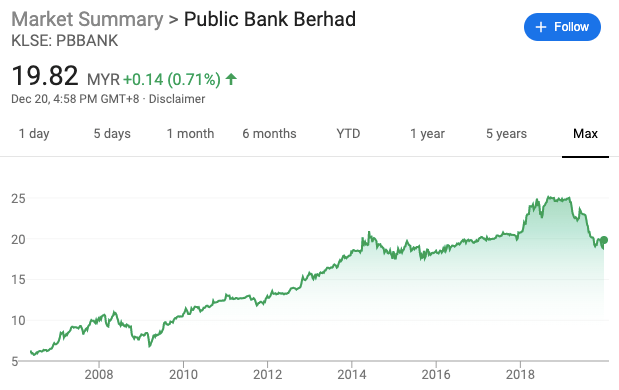

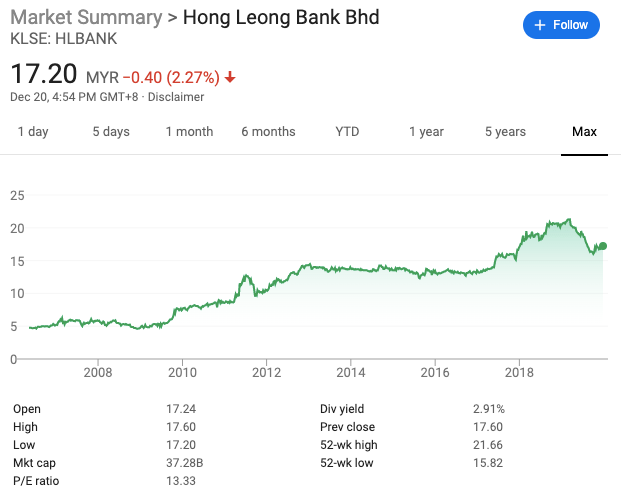

But that’s only part of the story. If anyone looked at the big bluechip companies that make up the KLCI index, you will find that the most of the declines are in the banks, especially Public Bank, the 2nd largest company on the KLCI.

The top 2019 declines in the value of KLCI companies (as measured by market capitalisation) are as follows. The reason I looked at their market cap is because companies with large market caps tend to move the KLCI index more when their share prices change.

| Listed Company | Market Cap (RM billion) | Share Price (%) | Earnings Change Q3 18 to Q3 19 (%) |

|---|---|---|---|

| Public Bank | -16.6 | -17.6 | -1.5% |

| Petronas Chemicals | -10.9 | -15.2 | -56.0% |

| Hong Leong Bank | -6.2 | -14.3 | -2.6% |

| British American Tobacco | -5.5 | -56.0 | -41.8% |

| Maybank | -3.3 | -3.3 | +2.1% |

Trivia note: the RM16b decline in Public Bank’s market cap is equivalent to one Sime Darby.

These companies have nothing to do with the US-China trade war. Additionally, Bank Negara OPR rates in Malaysia have been relatively stable, unlike what’s happening elsewhere in the developed countries.

Interestingly 3 of the 5 companies are non-Shariah compliant, and Malaysian funds have been actively shifting their money out from non-Shariah compliant companies to Shariah compliant ones. Notwithstanding the earnings drop of BAT, the drop of Public Bank and Hong Leong Bank share prices have far outpaced the minor drop in their earnings. Non-Shariah compliant companies are highly dependent on foreign funds to support their share prices. And we know that foreign funds have taken RM9b out from Malaysia so far in 2019.

If we exclude the effects of Public Bank and Hong Leong Bank from the KLCI, the total market capitalisation of all KLCI companies actually rose by RM11b, which isn’t that bad given the background of ‘US-China trade war, slowing global growth and negative bond yields’.

I suspect that large Malaysian funds are pushed to a corner to realise gains this year and hence dumped their old holdings of Public Bank and Hong Leong Bank shares which had given them immense unrealised gains over the years. Just check the 10 year price charts of their shares until 2019. Since foreign funds are generally pulling out of the KLSE, there’s nothing to support the prices of these shares.

Additionally as more and more Shariah compliant funds are launched, and people move their investments to these funds, non-Shariah compliant companies will see funds nett selling their shares.

What lies ahead in 2020?

Since 2013, the EPF has been drawing down on its reserves to sustain the dividends of above 6%. Barring accounting trickery, I would think that the situation is similar or worse for other Malaysian funds that did not diversify out of the Malaysian stock market.

It is highly possible that the EPF will announce a dividend that’s significantly lower than past years. It’s reserves were already negative as of the end of 2018 so its income for 2019 needs to come mainly from dividends and the active trading of stocks – there is little past unrealised gains to tap on this time.

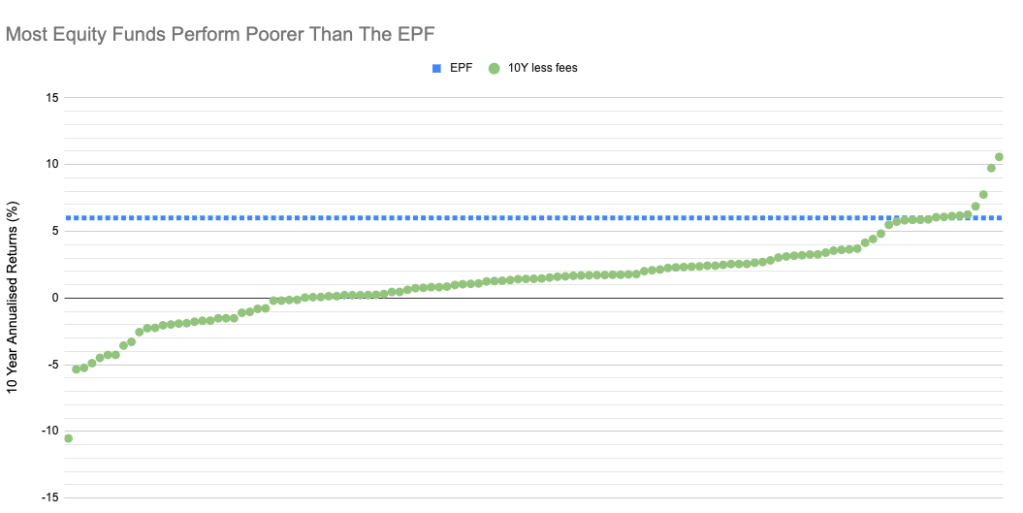

The good news is that even if the EPF declares a dividend of 5% for 2019, it still generates around 6% dividend on average over 10 years. Out of 119 equity funds listed on Fundsupermart that has been around for 10 years, only 9 have beaten the EPF, nett of their fees.

Putting it in another way, 92% of Equity funds provides less returns than the EPF (which is a balanced Equity/Bond/Property/Infra fund) over a 10 year time frame, when their fees are considered.

A potential problem for 2020 is that valuations of the US market continue to be high as plenty of growth expectations have been built into the prices of stocks. Additionally persistent low bond yields would eventually push people from bonds and into stocks, artificially inflating prices further. What this means is that funds that are just starting to invest overseas to improve their returns could be too late to the game. Many quality stock prices have gone higher than what the companies’ earnings could reasonably justify.

It will be hard to predict what will happen to the Dow Jones or the S&P 500 in the short term. There are 2 ways to go:

The first would be to ignore the noise and continue to invest periodically into the ETFs that track these indices. If you have taken care of your asset allocation in the first place, you would be comfortable temporarily losing 30% or 50% of your stocks investment in the event of a crash. Staying invested for the long term will allow you to eventually ride out the crash and join the next growth cycle.

The second would be to start putting your new investment money into ETFs that track value stocks. Value stocks are relatively still cheap and generally less affected by a market crash because the companies provide goods and services that everyone use during both good and bad times. There are no such ETFs listed on the KLSE unfortunately so one way would be to buy them directly from the NYSE via a stock brokerage account that allows foreign stocks trading such as the HLeBroking or CIMB iTrade. An example of such value ETF is the Vanguard Value ETF (VTV) which has an annual fee of 0.04%.

Whichever way that you decide to go, I wish you the best of luck in 2020!