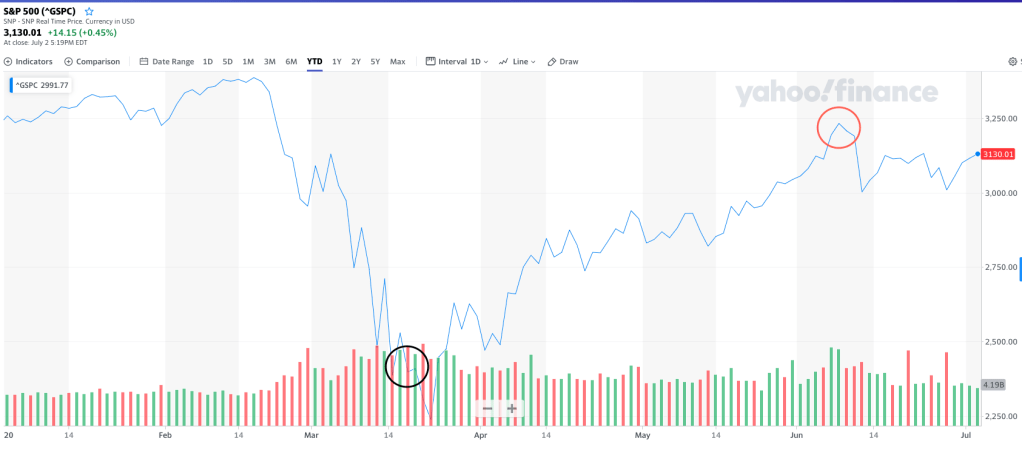

A lot has been written about the disconnect between Main Street (the economy and businesses) and Wall Street (the stock market) in the US. With record unemployment in the US, reduction in consumer spending and closures of businesses, it was surprising to see the S&P 500 and Dow Jones indices record a ‘V’ shaped recovery from end March to June.

Some may claim that the stock market is merely reflecting the temporary nature of the Covid-19 pandemic – that businesses will spring back to where they were in January once the pandemic is over. The problems with this claim are:

- After half a year, the pandemic is still accelerating globally. The peak of new daily cases in the US is still not reached. Therefore businesses will continue to be affected for months to come and their earnings will not recover to pre-pandemic levels any time soon.

- Most investment funds are fully invested at all times. When the stock market tanked in March, they are sitting on unrealized losses and do not have spare cash lying around to capitalize on the opportunity to buy on the cheap. Therefore it is impossible for these investment funds to push the stock market up on their own.

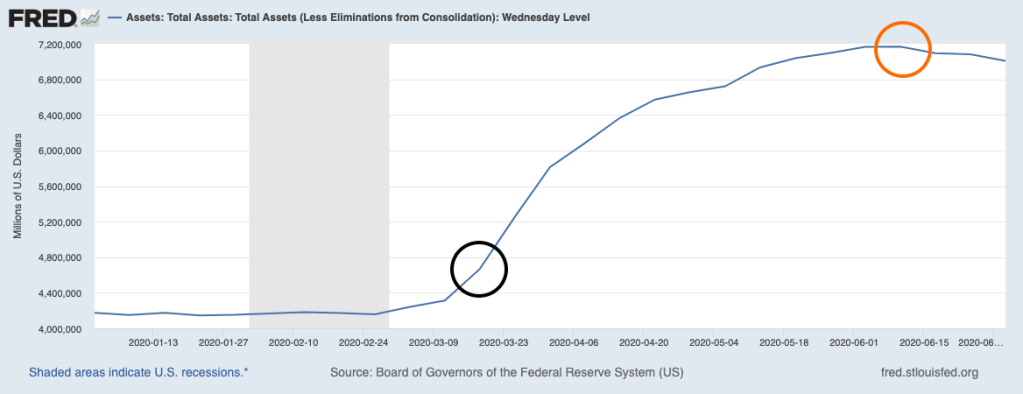

The key reason why the US stock market is up is due to the US Fed creating US dollars and using that to buy up bonds in the market. These US dollars are brand new, added directly into the monetary system, and not backed by any collateral. Around $3 trillion US dollars were created between March and June by the US Fed.

When the US Fed buys the bonds, the sellers of these bonds such as investment funds and other financial companies suddenly get the cash that that they sorely lacked to buy into cheap stocks. And that is how the stock market rose from end March to around June 8th.

In the last 3 weeks of June, the US Fed not only stopped buying the bonds but started to sell a bit of them back into the market. And when you look at the S&P 500, you also see that it has dropped slightly from June 8th to today.

So where does this lead us?

Contrary to what I previously thought, the US markets have recovered much quicker this round largely in part to the actions of the US Fed. The buying opportunity that presented itself in March may never return in the near term as long as the US Fed has its finger on the trigger.

The consequence of the Fed acting so quickly and at such furious scale is that prices of stocks and bonds have immediately become artificial, decoupled totally from the reality on the ground.

As companies reduce dividends to preserve cash throughout the pandemic, dividend rates will drop since the prices are being kept artificially high. Earnings per share will drop in Q2 and Q3 and this will result in elevated P/E ratios that will stay high for some time. And when you are regularly investing into stocks, the new money that you are adding is buying stocks at lower dividend rates and at higher P/Es.

The story isn’t great as well for bonds. As US Treasury yields are held near zero (0.67% at the moment for the 10 year note), returns from bonds will be flat for some time. This is because its price is unable to rise further (bond price goes up when the yield goes down and the US is not yet allowing for negative rates) and new bonds are offering coupon rates that are next to nothing. Low bond yields will be problematic for long term and conservative funds such as pension funds and insurance companies that depend on predictable cashflows.

You may wonder what about currencies? Should you just hold cash if there is nothing attractive to invest in? According to Ray Dalio, holding cash would be foolish as the US dollar will continue to devalue since there is no more room to cut interest rates and money printing is the only viable way out. But devalue with respect to what? At the moment, it would be with respect to stock prices which have been artificially inflated. Prices of everyday food and fuel are still the same.

But I have no idea how long this will continue to be the case. It is probable that any additional money printing by the US Fed will continue to feed US stock prices and then eventually property prices (due to the low interest rates). It is also probable that funds will eventually seek out the higher returns in emerging markets such as Malaysia since MGS bond yields are still comparatively high and the stock market is at multi-year low.

What about gold? Gold trading amongst investment circles has been driving up the price since the US-China trade war in 2019. The Covid-19 pandemic has only added fuel to push the price higher. It is interesting to note that overall demand and supply of gold have been relatively flat for 10 years. So supply and demand are not currently pushing up the gold price – trading amongst investors is. Nevertheless it cannot be denied that gold price trends upwards over the very long term – it is like the iPhone, no matter how high it is priced at, there will be buyers.

Maybe more people will rush for gold if an alternative currency emerges to challenge the US dollar. But at the moment there are no obvious winners since the Euro, Yen and British Pound are just as weak and the Chinese Renminbi is only held in 2% of the world’s reserve currencies.

So for now, it’s time to be patient again and reset my expectations for the US market.

Yeah I also wonder where should I put my money. Holding cash seems to be the way for now. I have 80% exposure in the US stock market. I wonder if I should sell off further. It’s a scary thing.

LikeLike

I guess selling would depend on how long do you plan to be in the US stock market and if you have bought individual companies (riskier) or a broad index based ETF (less risky). I’m planning to stay invested for the long haul mainly through the S&P 500 ETF so I’m prepping myself mentally to ride out the future volatilities. Selling will come when I’m retired or achieve financial independence 🙂

LikeLike

[…] and sold out in the darkest days of March, you would have missed the amazing recovery in stocks as central banks printed money by the trillions. Holding was better than selling, especially if you are holding onto a broad and simple index based […]

LikeLike

[…] When Covid-19 struck in early 2020, there was an expectation that entire economies will be crushed. Stock prices plunged worldwide. Even oil briefly struck negative prices (the Western Texas Intermediate crude oil price was -$37/barrel at one point which is laughable because in 2022 we saw the oil price going above $100/barrel again). However, central banks then quickly slashed interest rates to help businesses and households with loans and printed money to resolve liquidity problems in financial markets and fund governments Covid-19 response programs. This immediately changed the expectations of the investors because central banks have again stepped into to save the financial world. Prices of assets all rose in tandem but the real economy still got crushed. Those who had invested in early 2020 reaped handsome gains through 2021 even when the economy was struggling through Covid lockdowns and supply chain disruptions. People started swimming in the sea without their trunks. […]

LikeLike