There are countless books and articles in the internet recommending ways to assess if a stock is worthy to be invested or not. In most cases, those sources talk about the stocks that do well and use them in their analysis to uncover the metrics that reveal a successful stock. I will do the opposite in this post by sharing some of my bad stock investments and what I learnt over the years from these mistakes. Although the stocks are listed in different exchanges, the lessons can be applied generally in any market.

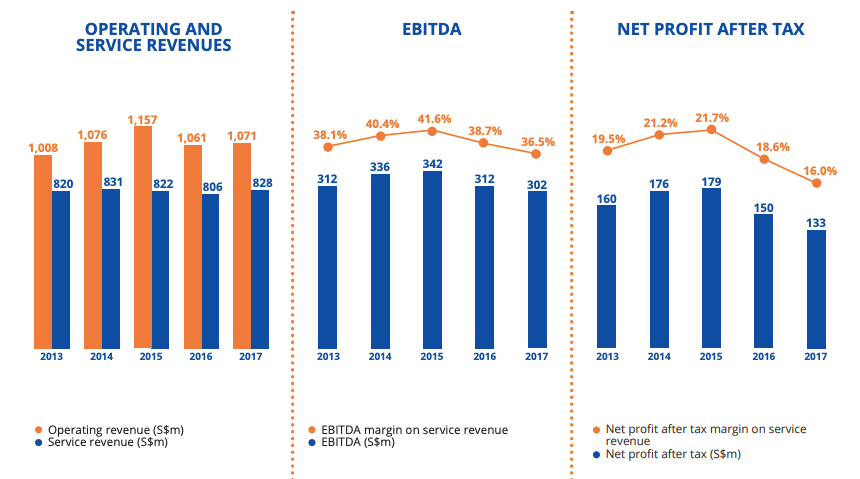

M1 Limited

M1 is a telecommunications company in Singapore that offer cellular and home broadband service. It is the 3rd largest telco by revenue after Singtel and StarHub. I first learnt of M1 when I visited Singapore in the early 2000’s and my phone sometimes roamed on their network. Although Singtel is the market leader, I decided to invest in M1 in the early 2010’s because I believed they offer a better customer service than the other providers and I considered this as their ‘moat’. My primary goal of investing in Singapore stocks then was for dividends as I wanted to diversify away from a depreciating Ringgit and Singapore is a strong market that is easy for Malaysians to access.

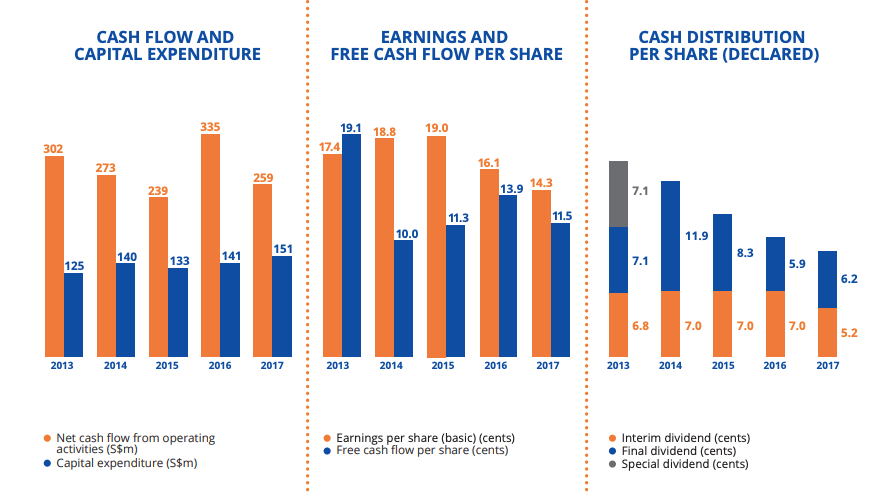

When I first bought into M1, it returned decent dividends of around 8%. It had strong cashflow that was fueling the dividends and revenue had been steady for many years. In addition to the strong dividends, the share price also climbed from around $2 in early 2010’s to almost $4 in early 2015. Just when it seemed that I had scored a winner with M1, the stock price started a multi-year decline back down to $2 in 2017 and then dropped even more.

Initially I didn’t understand the reason for the price declines. This was a solid business that had strong cashflow. As the price dropped I accumulated more shares. Sure there were signs that the average revenue per user was under pressure from competition but its management was also managing expenses to match the decline in revenue.

By 2016, it was clear that although the company was managing its cashflow well, its revenue was really under pressure from competition. This was back in the days when mobile operators had internet data price wars. They were slowly becoming ‘dumb pipes’ for the many apps that we started to use on our smartphones.

Rather than cutting my losses in 2016, I refused to believe that even as a ‘dumb pipe’ M1’s days were over. Singtel on the other hand, had already ventured out of Singapore by acquiring Optus, therefore expanding its addressable market from an overly saturated Singapore mobile market. M1 stayed with its domestic market. I stopped looking at the dropping earnings and hoped that the management had a good turnaround plan to address the declining revenue.

This is the first lesson: Be sensitive to when the business environment has structurally changed. Mobile data was becoming a commodity and mobile operators were in turn becoming ‘dumb pipes’. It’s ok to take losses when you are wrong. Doubling down on hope is a major mistake.

In the end my investment in M1 was ‘rescued’ by a Keppel and SPH joint venture that bought out the outstanding shares and privatised M1 Ltd in 2019. My consolation is that the joint venture offered a nice premium for the shares so I was able to recoup some losses.

Keppel Corp

During the days of the high oil prices between 2011 an 2014, oil and gas stocks were all the rage. This was the time when oil price was consistently above $100/barrel. However crude oil is a commodity and its prices moves in cycles. Soon enough, in mid-2014 the oil price crashed from over $100/barrel to below $30/barrel in January 2016. It was during this period of turmoil in the oil and gas industry that I decided to pick up stocks of Keppel Corp.

Keppel, like M1, is listed in Singapore and has businesses in oil rigs and support vessel construction, property, infrastructure such as data centers and investments. In 2013, which is prior to the 2014 oil price crash, its oil and gas related business contributed more than half of its $12.4 billion SGD revenue and two-thirds of its earnings. It had a strong engineering ‘moat’ in the construction of complex deepwater drilling rigs (think of the Deepwater Horizon disaster in 2010 and the technology needed to prevent that from happening again). I was certain that Keppel with the wealth of its engineering experience would be able to recover strongly from the oil price crash. Hence in 2015 I started to accumulate its shares after its price dropped from over $10 to just above $8.

This quickly turned out to be a mistake as I had read the oil and gas market wrongly. There was no rebound in oil and gas projects since the oil price stayed depressed for several years. Oil and gas companies dramatically cut expensive projects in 2014 and were only willing to proceed with projects that were more affordable and with quicker payback. That meant that the expensive deepwater drilling rigs that Keppel built were no longer needed. The engineering ‘moat’ quickly became irrelevant. The massive earnings from its oil and gas business from 2013 was almost wiped out by 2016.

Foolishly, I had poured in good money to average down my buying price of Keppel shares. Keppel shares slipped below $6 in 2016 and is just above $5 today. I finally exited my investment in Keppel in 2020 convinced that the oil and gas business is a sunset business and that Keppel is never going to be able to replace its past oil and gas profits with profits from its other businesses.

This was a lesson that took me 5 years to learn. The second lesson is: investing in a sunset business is unwise, even if you think you got in at a bargain price. When Keppel’s share price tanked after the oil price crash I thought that this was a great opportunity to own a wonderful bluechip company. But the 2014 oil price crash had changed the oil and gas industry forever and the latest price crash in 2020 has only accelerated their move out of oil and gas and into renewables and energy trading.

HeveaBoard Berhad

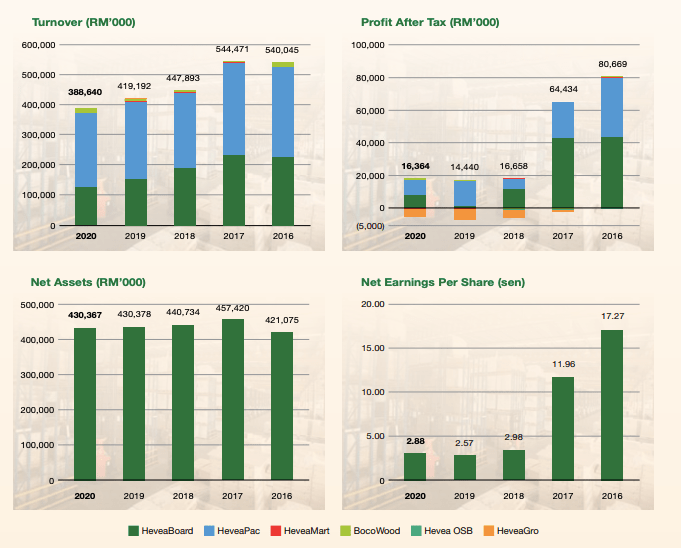

HeveaBoard is a primarily particleboard maker in Malaysia. The particleboards that it manufactures is also turned into ready-to-assemble furnitures. On the side, it has a small business in growing king oyster mushrooms with waste wood chips generated by its main businesses. HeveaBoard’s particleboard is of high safety quality which it exports to markets like Japan. It is run like a family business with the son of the founder currently the Group Managing Director. After listening to various interviews of the Group MD and also studying its business I decided to buy its shares in early 2016. This of course, had to the be the time when the share prices were at their all time highs. From late 2017 to today, the share prices and profits have slumped considerably.

Between 2016 and 2017, the share price went from RM1.20 to around RM 1.70. Turnover was increasing but earnings declined slightly. The Group MD sounded grounded, honest and transparent in his interviews, which added to my conviction in the company. In 2016 there was also a series of earthquakes in Japan, including the Fukushima earthquake that crippled a nuclear power plant. The rebuilding of homes in Japan was expected to deliver further earnings to HeveaBoard.

Source: HeveaBoard 2020 Annual Report

However things turned south in 2018. The company was hit hard by foreign labour shortages in Malaysia as the Ringgit had weakened substantially from 2013 to 2016. Back in 2013, 3 Ringgit could buy 1 USD. By 2016, 4 Ringgit was needed to buy the same 1 USD. A Malaysian salary was starting to look less attractive to these foreign workers. By late 2018, HeveaBoard lacked enough workers to maintain the production rate of its factories. It started to lose its economies of scale and profit margins. I, of course, thought this was a temporary problem that would eventually be resolved by the government through some form of industry aid or subsidy. I did not realise this was a structural problem that would not be resolved even to this day.

There are several lessons to this investment. The third lesson is: Management trustability is important but it is not a business ‘moat’. During the period of downturn, HeveaBoard’s management tried to diversify by cultivating and selling king oyster mushrooms. However it was not enough to mitigate the losses from its main businesses. The fact that their main businesses could be so easily threatened by the supply of foreign workers showed that they did not have a strong ‘moat’ and they did not have the technology to automate low skilled tasks. A weak business with strong management is like a big sailing ship stuck at sea with no wind – it will not be going anywhere.

The fourth lesson is: Be patient with your winners but less so with your losses. HeveaBoard reported their problems with the supply of foreign workers for many quarters. I took too long to come to my senses that this problem was not a temporary one before I cut my losses. I was too patient in hoping that the situation would turnaround for the company even though it was clear that neither the company nor the government was doing anything effective to resolve the issue. When the future profitability of a company is structurally affected, I should exit the investment quickly.

I hope these few lessons that I’d learnt over the years would come useful in your stocks investing journey.