From the perspective of investments, properties have plenty of undesirable traits. It’s expensive and typically you will be unable to buy it outright – you pay part of it as downpayment and then borrow the remainder from a bank.

When Buying, Set Aside More Than The Downpayment

The downpayment can be quite substantial – usually 20% of the purchase price but if you qualify, you may be able to borrow more from the bank so that a 10% downpayment suffices. If you purchase the property from the secondary market, you have to also settle legal and stamp duties which will come up to 5% of the property value. And then you have to think about furnishing or even repairing/renovating the property, which can come up to another 10%-20% of the property value. This means that your initial capital outlay, including the downpayment, can already reach 35%-45% of the purchase price. How long will it take to save up this kind of money?

When Servicing Your Monthly Payments, Try To Lower The Interest Amount

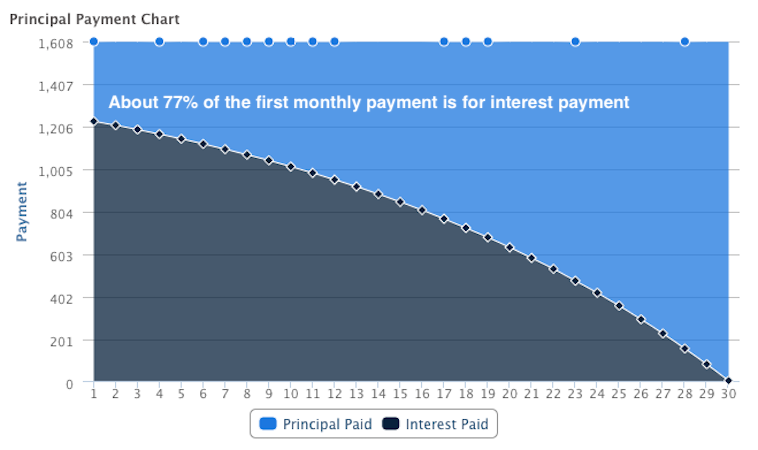

Since the bulk of the money needed for the purchase is borrowed, you have to repay the bank the principal borrowed with interest. The interest itself can be quite substantial if you add it up over time. In the initial years, most of the mortgage payment will go towards paying the interest (~77% in the first payment). It is only when the mortgage balance reduces to about 2/3 of the original loan that you will start paying less for interest than for the principal.

There are ways to reduce interest costs with the bank. One way is to take the highest amount of loan that you can qualify for and for as long a duration as possible even though you can afford to pay a larger downpayment.

For example, if you have saved enough for a 20% downpayment, try to apply for a 90% loan nevertheless if you are able to qualify. As you are servicing the loan, put down the 10% to pay down the principal. This immediately reduces the interest calculated from next month onwards and also reduces the duration of the loan. The amount of interest saved this way is actually more than if you had tried to get an 80% loan. Malaysians also have the option of using their EPF Account 2 for the same trick.

Additionally these days there are flexible home loans that would allow you to withdraw the excess payments during times of financial emergencies. Just be aware that the interest calculated would go back up once the excess payments are withdrawn.

Another way to reduce interest cost is to refinance the loan with another bank should interest rates fall. Just be careful of any related fees and also avoid the penalty from breaching the minimum lock in period of the loan.

Through a combination of tactics to reduce the interest costs and make excess payments from time to time you can reduce the duration of the loan. Just to give an illustration, simply paying 50% more in monthly mortgage will halve the loan duration and reduce the total interest payment amount by over 50%.

Take A Few Years Before You Upgrade To Another Property

You could work out the returns for owning a home and you will find out that there are many factors. However, it will be safe to assume that the chances of making a loss is quite high if you do not plan to stay longer than 5 years. The main reason is the costs that are unrelated to the property price that you would pay when you acquire it, ie furnishing, legal, repair and renovation costs. It takes years to recoup them through the capital appreciation of the property.

When the time is right (eg 10 years or so), you can consider upgrading to a bigger home when you are financially able to afford a larger mortgage. Just as there are associated costs when buying a property, there are associated costs when selling a property. Hence, it is usually not beneficial to upgrade to a new home in short periods of time.

Selling A Property Will Take Time And Money

When you sell a property you normally need to engage the services of an agent, who will take 2% of the eventual selling price as commission. Depending on how long you have held the property, you will also need to pay a capital gains tax, which is normally withheld from the selling price by the lawyer.

Depending on its location, it may take months before you find a prospective buyer. Even if you have a ready buyer, the whole transaction will take months to complete. So it’s an illiquid asset, something that you cannot count on if you need quick cash.

But A Home Is Different From A Normal Property Investment

As an investment class, properties can be risky if you make a mistake. But if it is for your home then it’s a worthy investment for your peace of mind. Now I’ll explain why, despite all the costs and disadvantages, buying a home is always worth it and under what circumstances.

A home is unlike a property investment. The criteria for choosing a home is quite personal and different from an investment property. A home can be a safe and comfortable place to raise a family. It can also be a place that is close to friends or other family members. More importantly buying a home means being comfortable to stay in the place for some number of years. If you plan on moving around, then continue to rent instead.

In your eventual golden years, you would want to enjoy your retirement funds and do the activities that you want. And the key thing to that is to greatly minimise, or even eliminate, your regular ‘big rock’ expenses such as rent and loan repayments. Instead your retirement funds should be channeled to your ‘variable’ expenses and used to maintain or even increase your experiential lifestyle if you can afford it (take a first class long haul flight if you’ve never done it, dine in a Michelin stared restaurant, etc).

As a counter argument, it is possible to overcome this if you have an investment portfolio that provides sufficient returns that cover all your expenses during your golden years. But nothing provides the peace of mind like a roof over your head that’s unencumbered and fully yours. Let your investment returns take care of the other unavoidable stuff like maintenance and taxes/assessments.

When you are old, the last thing you want to worry about is paying monthly rent or home loan payments. And getting a home and paying it off before you retire is the key to that. As you work on building up your investments so that you can afford your first home, you should also be building up your retirement fund. The next post will discuss your next layer of the ‘asset allocation model’ which is long term savings, aka retirement savings.

[…] Once you have built your personal financial safety net the next step is to take additional risks and build your investment plan. More on that in the next post. […]

LikeLike

[…] By taking the additional risk of investing in shares you accelerate the growth of your investments as hard as you can while spreading out the risks through diversification. In a few years’ time, you should have gained enough to meet one of your goals, like buying a home. […]

LikeLike

[…] your day to day savings account, why you need an emergency fund, why you should seriously consider buying a house as a home and finally know your options to build the foundation of your retirement […]

LikeLike

[…] in 2018 I wrote about owning a home as part of one’s asset allocation strategy. A home is a unique asset because you can […]

LikeLike