This is the fifth post in a series of posts that talk about building up your personal finances. If you have followed the series you would learn how much to keep in your day to day savings account, why you need an emergency fund, why you should seriously consider buying a house as a home and finally know your options to build the foundation of your retirement fund.

Everything up to this point builds a strong foundation for you to really start growing your nett worth. This means you can take on more and more risks to grow your savings and investments without worrying about your cashflow needs. You can afford to take a very long view about your investment returns and not worry about the temporary ups and downs of the markets. You have no immediate need for the money invested and more importantly you should take the opportunity to enjoy living in the present without worrying too much about the future.

Fixed Income Investment

In this post, I will start with the investment that offers the lowest risk – fixed income investment.

Fixed Deposits

For Malaysians this will be quickly recognised as savings in fixed deposits. With fixed deposits, you lend a bank a certain amount of money and in return, the bank agrees to pay you back the money (ie principal) together with a fixed interest amount after an agreed amount of time. You also promise not to renegade on this arrangement by demanding the money back earlier than agreed, otherwise you would forfeit all or part of the interest earned.

There is essentially zero risk to your money in fixed deposits as long as your total savings and fixed deposits with interests with the bank is less than RM250,000. A government insurance for depositors (PIDM) provides this protection. If you plan to have more than RM250,000 in savings and deposits, then split it between several banks.

Online banking these days makes it very easy to set up and monitor fixed deposits. You can easily create a fixed deposit account and fund it from your savings account all from the comfort of your home.

Set it up to auto-renew with the interest added to the principal amount upon maturity so that you can benefit from compounding interest.

Historically, a 1 year fixed deposit interest rate is between 3% and 4%, which is just above the official inflation rate from the (useless) Malaysian Consumer Price Index (CPI). We all know that personal inflation numbers can be much higher since it depends on location, age and lifestyle.

Bonds

The government, statutory bodies and companies raise funds from time to time and one way is to borrow money from the public through bonds. Essentially an ‘I owe you’ paper, bonds are promises from the borrower to repay the borrowed money with an agreed interest (otherwise known as coupon in bond-speak) typically over a number of years. However, unlike fixed deposits, bond papers can be further sold by the lender to other interested parties.

Being able to buy and sell bond papers means that the prices of bonds can fluctuate up and down based on supply and demand. The prices also depend on the financial health of the company or the country’s economy. Since the interest, or coupon paid by the borrower is always the same, when the price of a bond goes up, its yield will go down accordingly. Similarly when the price of a bond goes down, the yield will go up.

Just to take a simplistic example, suppose a bond has a (face) value of $100 per unit and offers a coupon rate of 5%. This means that the borrower will pay $5 for each unit to the bond holder every year. If the bond is sold to another person at a higher price of $110 per unit, the borrower will still pay $5 for each unit to the new bond holder each year. For the new bond holder who has paid $110 per unit, it would appear as if the yield of the bond has dropped to 4.5%. (The actual bond yield calculation is more complex than this but the general relation between the price and yield is the same)

For someone who buys bonds and holds them all the way to maturity, then all this price/yield movements may seem irrelevant. But bonds are riskier than fixed deposits because you can be exposed to the possibility that the borrower is unable to pay the coupon on time, or the face value of the bond when it matures. Bonds are also not insured by the PIDM.

As an example, Tenaga Nasional (TNB, the electric company in Peninsula Malaysia) could have issued bonds to borrow money in order to build really expensive power plants. Power plants initially require a lot of money (capital) to build but the company has a monopoly in supplying electricity to consumers. Hence, initially, the lender has some comfort with the ability of Tenaga Nasional to pay the coupons.

Now what happens if one day the government decides to reduce the electricity tariff to consumers without any compensation to Tenaga Nasional? Or perhaps the government may decide to break the monopoly and let other private companies supply the electricity directly to consumers? Suddenly, it looks like there is some small possibility that Tenaga Nasional may have trouble paying the coupon and/or the bond face value when it matures.

Frightful lenders may decide that the risk is too much and sell their bond papers to others who may have bigger risk appetite. They may even sell their bond paper at a loss. So it is possible to have a loss with bonds.

You can gauge the risk of the bond by looking at its rating. Agencies in Malaysia like RAM will assess the financial capability of the bond issuer and then give the bond a rating. The best rating is AAA, which is nearly risk-free. The lowest rating is D… for default. The riskier the bond, the higher its yield would be in order to attract bond buyers.

Certain bonds can be purchased like a stock through your brokerage account or by physically visiting banks. But it’s easier for normal folks to buy them through mutual funds or or an exchange traded fund (ETF) such as the ABF Malaysian Bond Index. Buying them through mutual funds or an ETF allows you to buy bonds at smaller chunks or lots and the funds will split them over a collection of bonds so you also reduce your risks by diversifying over different types of bonds with different ratings. One good place to start searching is the fundsupermart.com

It’s important to check the rating distribution of the fund by looking at its annual report. For example a bond mutual fund may appear to provide very high yields but it could consist of high risk bonds on the verge of default.

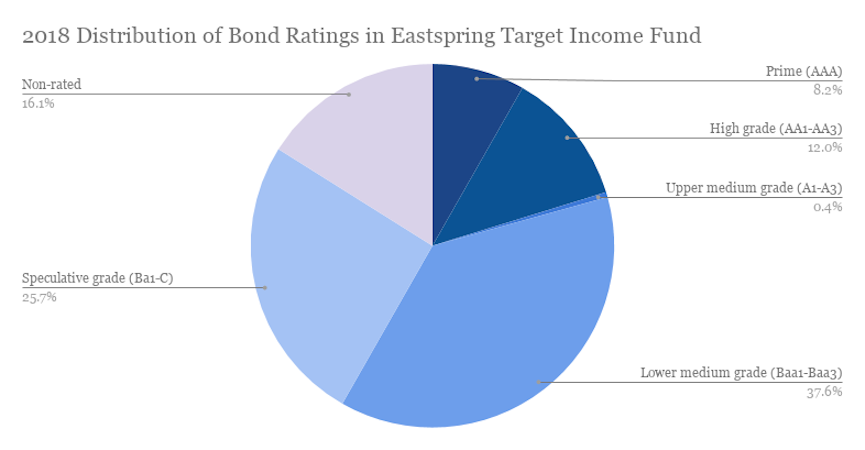

As an example, below is the distribution of bonds by ratings held by the Eastspring Investments Global Target Income Fund as of the end of May 2018. Only 20% of the bonds are in upper medium grade of A3 and above. In 2017, the fund gave a return of 10.6%. But in 2018, it eventually returned -4.09% as bond prices dropped because the rising interest rates in the US put pressure on the ability of corporates to service their bonds.

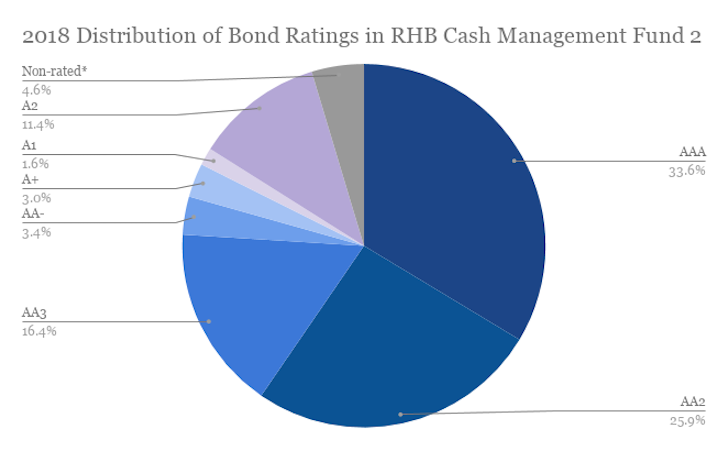

As a contrast here is the distribution of bonds by ratings held by the popular RHB Cash Management Fund 2 as of March 2018. The fund has 2 strategies: never buy bonds below the rating of A2 (which means only buy bonds with upper medium grade and above quality) and only buy bonds that will mature within a year. Indirectly, this puts it in competition with traditional 1-year fixed deposits. The return of the fund in 2018 was 3.49% but if you take into account the management fee of 0.4%, this then drops to 3.09%, which is quite poor compared to the risk-free fixed deposit.

Beware of Fees

As seen in the RHB fund above, it’s important to check how much is the annual management fee, sales fees and redemption fees. As bond funds typically return very little (best bond funds in 2018 return 5%-6%, worst ones lost 9% and more) high fees, will severely hit your returns. Remember, these fees are always charged even when the fund loses money.

As an example, the top bond fund in 2018, AmDynamic Bond returned 6.39% but has an annual management fee of 1% and a redemption fee of 1%. This means that the fund manager takes away over 15% of your profit for the year leaving you with 5.39%. If you sell (redeem) your units, then you incur another 1% charge leaving you with 4.39%. This put it comparable to some 1-year fixed deposit promotions offered by banks which offer zero risks.

Comparatively the 2nd best bond fund of 2018, the Nomura i-Income Fund returned 6.01% and has an annual management fee of 0.25% with zero sales and redemption fee. This means that if you sell (redeem) your units at the end of 2018, you will earn 5.76%, which is clearly better than AmDynamic Bond. Alas, this fund is only available to high net worth individuals as it is what’s called a wholesale fund.

So Which Is Better, Bonds or Fixed Deposits?

The answer to this question depends on how much return you want to get out of your investments and how much risk you are willing or supposed to take based on your age.

When you are young, you can take on relatively high risks since you have a very long term investing horizon in front of you. In such cases, both bonds and fixed deposits would not be in your investment portfolio. You may only hold them as your emergency savings fund instead. You would go for investment types that offer a much higher return in the long run.

But if you have retired in your golden years or cannot stomach even an ounce of loss in your investment, then you should put a big chunk of your investments in fixed deposits, bonds and a bit in diversified stock indexes (more on diversified stock investment in the next post). For bonds, pay close attention especially to the management, sales and redemption fees and focus on funds that have low fees. If you keep losing money to these fees, you may end up with the same or poorer return compared to fixed deposits.

Am not a Malaysian but This article is very informative. Thanks

LikeLike