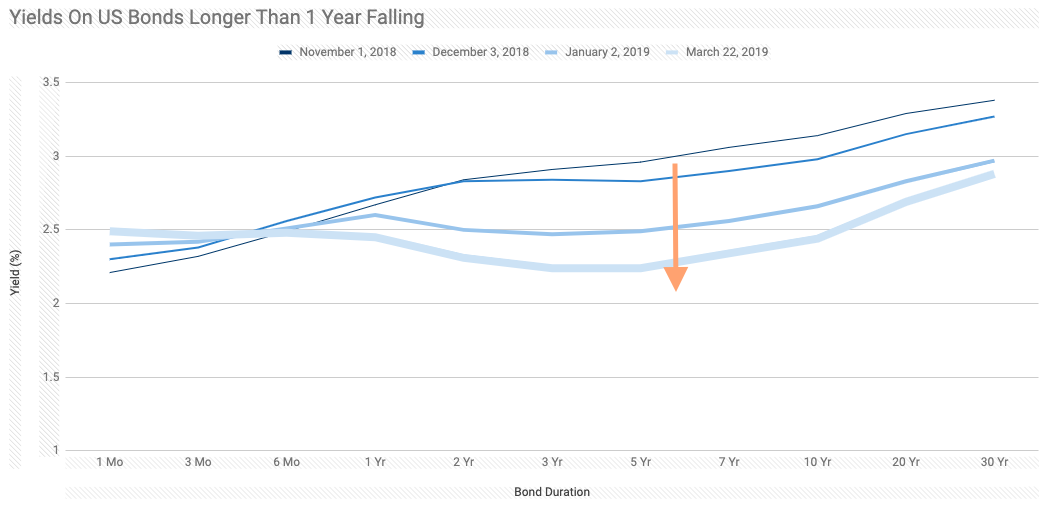

Since December 2018, something rare has been happening to the US treasury bond yields and the trend is still continuing to today. The yield on bonds with durations longer than 1 year have been gradually dropping while the yield on bonds shorter than 6 months have slightly nudged upwards. This has finally resulted last Friday (22 March) in the yield of the 10 year bond (2.44%) dropping below the yield of the 3 month bond (2.46%).

Bond Basics

A bond is an ‘I-owe-you’ paper issued by a government or corporation that wishes to borrow money from the public. The government or corporation then promises to pay interest (ie coupon) periodically on the borrowed money and repay the original borrowed sum (ie principal or face value) after an agreed period of time (eg 3, 5, 7, 10 years).

Just like fixed deposits, and under normal circumstances, the longer the duration or tenure of the bond, the higher its coupon rate will be. Imagine yourself lending money to another person that you know superficially. You may perceive some risk in the borrower of not being able to repay the money. If the borrower promises to repay the money as soon as possible, the risk may appear less. Similarly, if the borrower says that he or she can only repay the money in 10 or 20 years, you may get a feeling that the risk is higher. You would want to be compensated with an interest rate (or coupon rate in bond speak) that is commensurate with the risk that you are taking.

Unlike fixed deposits however, bond papers can be sold to other interested parties. The buyer may purchase the bond papers at a higher price than what the seller originally got them for if he or she has greater confidence in the ability of the government or company to pay the coupon and face value of the bond. The reverse can be true if the confidence in repayment drops.

Since the coupon payment is fixed, as the bond becomes more expensive, the reward from its coupon payment becomes relatively diminished. The ratio of the coupon payment to the bond price is known as its yield. In summary, as the bond price goes up, the yield of the bond goes down, vice versa.

The Yield Curve

Typically, shorter duration bonds get lower yields than longer duration bonds. If you plot the yields of bonds with different durations on a chart you would see more or less a straight line going upwards (y=mx+c type). This chart is known as the yield curve.

As economic situation changes (inflation, unemployment rates, GDP etc), the shape (ie slope) of the yield curve changes. What has happened recently is that there are concerns about the US economy that causes more people to buy longer duration bonds than shorter duration bonds. In other words, they are seeing more economic risks in the short term than in the long term.

An extreme situation happens when the demand for long duration bonds becomes so intense that its yield drops below that of short duration bonds. Drawing the analogy with fixed deposits, this is like a bank offering you a 3% interest rate for a 5 year deposit vs a 4% interest rate for a 3 month deposit.

It’s not a rational situation but it happened last Friday 22 March when the yield of the 10 year US bond dropped just a tad below that of the 3 month bond.

Recession Ahead?

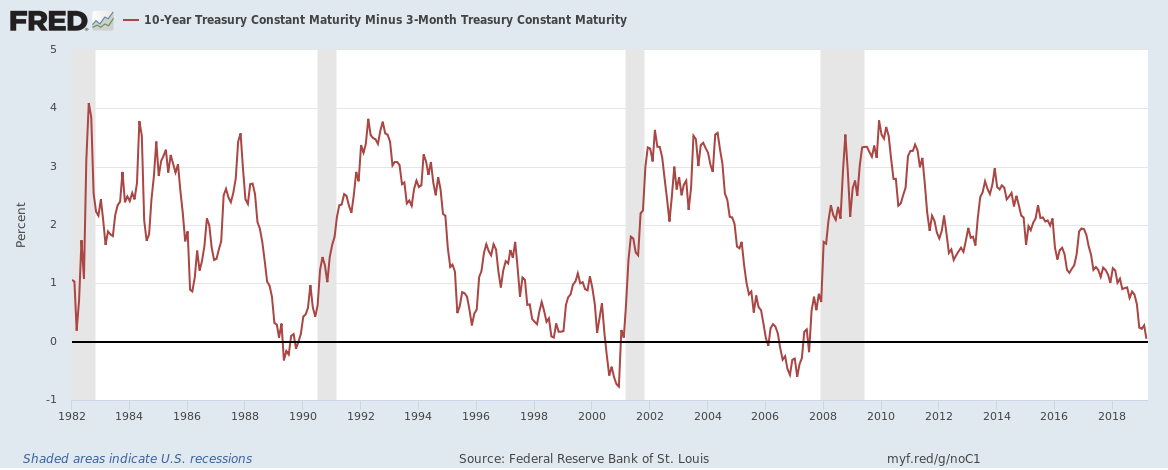

In the last 30 years, there have been 3 recessions in the US. All 3 were preceded by the yield of the 10 year US bond dropping below that of the 3 month bond. If we are to believe that the (bond) market knows best, then it would seem that they were right in those 3 times.

As markets are cyclical it’s not a matter of if but when a recession will hit. So far the signs are showing that one is looming probably 6 months to a year away.

Does This Translate To Panic In The Stock Market?

Possibly. Historically, periods of US recession have coincided with periods of declines in the S&P 500, which isn’t surprising.

If you are into individual stocks investing, it would be a good strategy over 2019 to raise or preserve cash so that you can average down your buying costs when the decline happens.

If you are into index funds and investing regularly for the long run, then you don’t have to react too much. As the stock indices climb, you should be buying less units anyway as the prices go up. And when the market eventually declines, your regular investments should start buying more units which should benefit you once the decline reverses.

[…] had some worries in 2019 that a recession was looming when the US bond yields started inverting in March 2019, which had been a reliable indicator from past history. This then prompted the US Fed […]

LikeLike