It is not uncommon to hear from those who are tired of their jobs that they wished they could simply stop and do something else that they might enjoy. However, reality usually strikes them in the form of bills and/or mortgages to be paid. So they simply suck it in and continue with the drudgery of their working lives.

The funny thing is that nothing really stops people who are disenchanted about their work from simply changing jobs or picking up a new skill or trade. It could be the struggle of starting all over again in a new work environment or the comfort of a good salary or unbeatable benefits that holds them back.

A Solid Financial Foundation Gives You More Options

Whatever the case may be, having a solid financial foundation makes career changing decisions easier to make. This means not having to worry if you are without a salary for a short period of time as you switch jobs or allowing you to settle for a dream job that offers a lower salary but is more fulfilling personally.

The ultimate financial status is of course having complete financial freedom when you can actually go on paying all your bills and expenses without having to rely on any salaried jobs. Getting a job and receiving a salary then becomes a nice to have hobby; it is no longer a need.

Ironically, all of us will be forced one day into this situation whether we are ready financially or not. That day is called ‘retirement’. In Malaysia, that will be when you reach the age of 60. Ideally you do not want to be caught in a situation where you are forced to work for income when you are past the retirement age.

Don’t get me wrong though – it’s perfectly fine and perhaps essential for the mental well-being of everyone to continue having some kind of work. But in an ideal world, retirees shouldn’t have to work because they are forced to rely that income to continue living.

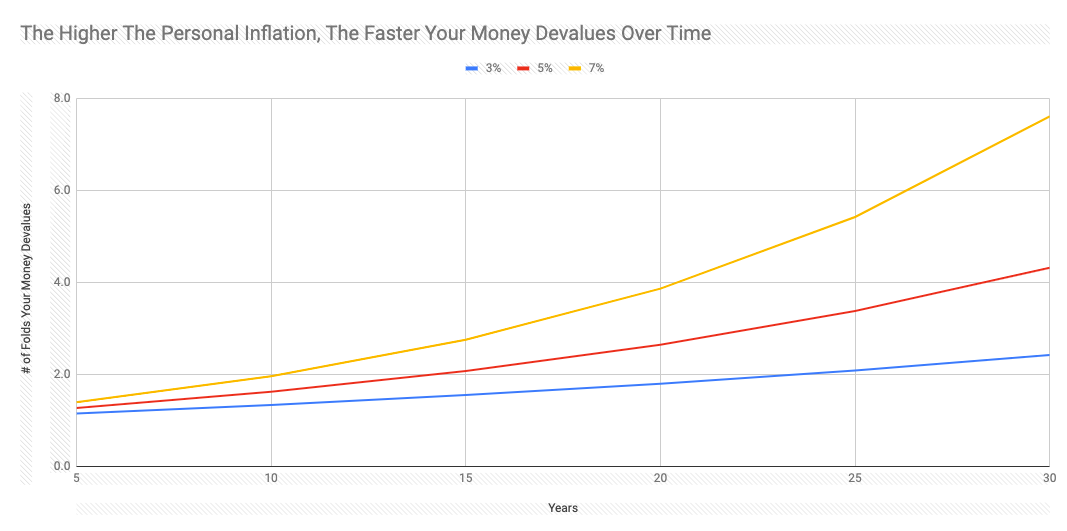

Financial Freedom Is Very Expensive

The numbers involved in getting to financial freedom can be really daunting. Generally they depend on:

- Your aspired lifestyle – how much do you need to live a meaningful life?

- Your personal inflation – how much do the stuff that you buy go up in price year to year? This is very personal and can be very different from the country’s official inflation figures.

- Your age – how long do you have to build up your investments?

- Your commitments – do you have children and what are your plans for their education? Do your parents require regular medical care and equipment?

Let’s start by targeting an age when you think you need to be financially free, say 60 years old. By then it could be safe to assume that your children have graduated from college or university and are financially independent on their own. You can then say that you will need perhaps 50% of what you are spending today to live a meaningful life. Let’s call this your retirement lifestyle expenses and as a wild example, let’s say this amount is RM3,000 a month in today’s money, or RM36,000 a year.

As inflation devalues money over time, you will need to inflate this number into the future by the number of years that you have between now and 60. The mind is quite poor at imagining exponential trends but as an example, if you have a personal inflation of 5%, you will need 3.4 times of today’s money’s worth if you have 25 years to 60 years old. This means that the RM36,000 annual need in today’s money is actually a RM122,400 annual need in 25 years’ time.

Never forget to plan for inflation

You can use a similar approach to figure out how much you will need for your children’s education in the future. Look at how much the tuition fees and living expenses cost today and then inflate the amount by the number of years your children have before they enter college or university. Education costs are inflating around 5% to 10% each year.

The numbers can be shocking when you add them all up. Blame it on inflation.

Saving Money Alone Cannot Bring You To Financial Freedom

Just by looking at the numbers, it is probably clear that savings alone cannot get you to where you need to be in order to be financially free. It is also probably just as clear that you would need a plan to invest your savings so that it can grow exponentially faster to counter the effects of inflation.

One way to think about this is to ensure that your wealth grows at least as fast as the rate of your personal inflation plus the amount that you would need each year. That way, your wealth essentially never depletes even as you withdraw an amount that increases with your personal inflation rate each year.

Here’s an example to illustrate how this can work. Suppose that you need RM3,000 a month or RM36,000 a year to live a meaningful retirement life. You could also move to a state or district with a lower cost of living to get the best value out of that RM3,000 a month. Assume also that your personal inflation rate is 3% so the monthly RM3,000 that you need, grows to RM3,090 the following year. Every year, the need goes up by 3%.

If you have a net wealth of RM800,000, you could withdraw 4.5% of that at the start of each year to ‘pay’ yourself the RM36,000 (800k x 4.5% = 36k). The remainder of your wealth (RM800,000 – RM36,000 = RM764,000) would continue to be invested in a LOW COST diversified index based ETF that would provide an average net return of 8% each year (8% is at least more than the sum of 3% inflation and 4.5% withdrawal). By the end of the first year, the RM764,000 should grow back up to RM825,120. At the start of the following year, withdraw RM37,080 to ‘pay’ yourself. This amount is 3% higher than the RM36k of year before to account for your personal inflation. This leaves you with RM788,040 (RM825,120 – RM37,080) which would grow by 8% to RM851,083 by the end of the year.

Although this is an idealistic example, a strategy of measured withdrawal and staying invested will ensure that you will never run out of money despite rising costs due to inflation.

Seeing the initial amount of RM800,000 may already deflate the hopes of many reading this article. But there are several ways to solve this. As an example, if you invest RM900 each month into the same LOW COST diversified index based ETF with 8% net return, you can hit RM800,000 in 25 years. Additionally you could sell your home and buy a smaller but cheaper home to raise more cash.

The actual math involved is slightly more complex than this if you are planning for the future since all numbers would be inflated by inflation. But the strategy remains the same: use a higher return to fight the effects of inflation. This spreadsheet may help.

Light At The End Of The Tunnel?

Achieving financial freedom is possible with some frugality and a very long term view of planning and investing. In reality, everyone can take different paths achieving it because everyone has unique personal situations. In some years, investments can do very well but in other years, they may also suffer losses. The key thing though is to remain invested and set your sights for the long term.

The journey to financial freedom can be long and boring. However when you get there, the rewards can be totally worth it.